Investing in Stocks vs. Mutual Funds: Which is Better?

Dany M.

Stocks and mutual funds are common investments for people who want to grow their money. They're both good for building portfolios, but there's a lot of difference between how they work and what you can expect.

But which option is actually better? For the best investment choice, you need to know the main differences between stocks and mutual funds, including their pros and cons, risk and return, and more. Let’s take a closer look at each option.

Stocks vs. Mutual Funds: Overview

Stocks

Stocks, also known as shares or equities, represent ownership in a company. When you buy a stock, you become a shareholder and own a small piece of the company. Companies issue stocks to raise money for various purposes, such as expanding their business, funding new projects, or paying off debt.

The stock market is where stocks are bought and sold. It acts as an exchange mechanism that brings together buyers and sellers, facilitating the trading of stocks.

The two main types of stocks are common stocks and preferred stocks. Stocks can be further classified based on various factors, such as:

Company size (large-cap, mid-cap, small-cap)

Sector (technology, healthcare, finance)

Investment style (growth, value, income)

For example, blue-chip stocks are shares of well-established, financially stable companies with a history of consistent growth and dividend payments. Some examples of blue-chip stocks include Apple (AAPL), Microsoft (MSFT), and Johnson & Johnson (JNJ).

Investors buy stocks to earn a return on their investment, either through capital appreciation (an increase in stock price) or dividends (a portion of the company's profits distributed to shareholders).

Mutual Funds

Mutual funds are investment vehicles that combine money from many investors to buy a diverse range of securities, like stocks and bonds. Instead of investing directly in individual companies, mutual fund investors pool their money together, allowing them to access a professionally managed portfolio.

Mutual funds come in various types, each with its own investment strategy and asset allocation. Some common types of mutual funds include:

Equity funds: Invest primarily in stocks

Fixed-income funds: Invest in bonds and other debt securities

Balanced funds: Invest in a mix of stocks and bonds

Index funds: Aim to mirror the performance of a specific market index, such as the S&P 500

Sector funds: Focus on specific industries or sectors, such as technology or healthcare

Investors can purchase mutual fund shares directly from the fund company or through a broker. The price of a mutual fund share is determined by its net asset value (NAV), which is calculated by dividing the total value of the fund's assets by the number of outstanding shares.

Key Differences Between Mutual Funds and Stocks

Stocks vs. Mutual Funds: Ownership Structure

When you invest in stocks, you become a direct owner of a small portion of the company, known as a share. This ownership entitles you to certain rights, such as the ability to vote on important company decisions and the potential to receive a portion of the company's profits through dividends. The number of shares you own determines the extent of your ownership in the company.

In contrast, when you invest in a mutual fund, you don't directly own the individual securities held by the fund. Instead, you own a portion of the fund itself, which in turn owns a portfolio of securities. This means that your ownership is limited to the mutual fund shares you hold.

For example, if you buy shares of Apple (AAPL) stock, you become a part-owner of Apple Inc. and have the right to participate in shareholder meetings and vote on certain corporate matters. However, if you invest in a mutual fund that holds Apple stock, you don't have any direct ownership or voting rights in Apple – your ownership is in the mutual fund.

Stocks vs. Mutual Funds: Diversification

When you buy individual stocks, you're investing in a single company, which can be risky. If that company performs poorly, your investment could suffer significant losses. Instead of holding a more concentrated portfolio, diversifying can help lower volatility and improve risk-adjusted returns.

Mutual funds, on the other hand, offer instant diversification by investing in a wide range of securities, potentially including hundreds of stocks and bonds. This spreads your risk across various assets, sectors, and industries, reducing the impact of any single security's poor performance on your overall portfolio.

Stocks vs. Mutual Funds: Management

Investments are a big deal, and you want your money to be in good hands. With individual stocks, you're the one calling the shots. You decide which companies to invest in, when to buy, and when to sell. While this level of control can be appealing, it also means you're responsible for researching companies, monitoring your investments, and making decisions based on your analysis.

Mutual funds, on the other hand, are managed by professional fund managers. They're responsible for selecting which stocks, bonds, or other assets to include in the fund's portfolio, and they continually monitor and adjust the portfolio as needed.

Of course, professional management does come at a cost. Mutual funds charge fees, which can eat into your returns over time. And even with expert management, there's no guarantee that a fund will outperform the market or meet your specific investment goals.

Stocks vs. Mutual Funds: Minimum Investment Requirements

Both tocks and mutual funds have different minimum investment requirements.

With stocks, you can start small. If you want to invest in a company like Amazon (AMZN) and the stock is trading at $3,000 per share, you can buy fractional shares. This means you can invest as little as $1, and you'll own a small piece of a share. Many brokerages, like Charles Schwab and Fidelity, offer fractional shares, making it easy for anyone to start investing in stocks.

On the other hand, the minimum initial investment for most retail mutual funds in the US is between $500 and $5,000. Some mutual fund companies offer even lower minimums for certain types of accounts, such as retirement accounts or automatic investment plans.

However, some mutual funds have no minimum investment, while institutional class funds and hedge funds may require at least $1 million or more. For example, the Schwab Fundamental US Large Company Index Fund has no minimum investment.

Stocks vs. Mutual Funds: Liquidity

Liquidity refers to how quickly and easily you can convert an investment into cash without affecting its price.

Stocks are generally more liquid than mutual funds. When you own individual stocks, you can sell them anytime during market trading hours. This means you can access your cash quickly if you need it.

Mutual fund shares, on the other hand, are only priced once a day, after the market closes. If you put in a sell order for your mutual fund shares during the day, you'll get the price at the end of the trading day, known as the net asset value (NAV). You'll typically receive your money within a few business days.

Some exceptions are worth mentioning:

Some money market funds offer high liquidity but generally lower returns.

During market stress, mutual funds may implement redemption gates or fees to manage liquidity.

Your choice between the two may depend on how quickly you need access to your money versus your long-term investment goals.

Stocks vs. Mutual Funds: Fees & Charges

The trading commission is the main cost you will face when you buy stocks. But there is good news: many brokers now let you trade stocks without paying any fees. For example, as of 2024, popular brokers like Charles Schwab, Fidelity, and E*TRADE all offer $0 commission on online stock trades for U.S.-listed stocks and ETFs.

There may be other fees or conditions associated with certain types of trades or account activities. Always check the full fee schedule and terms of service for each broker to understand all potential costs associated with your specific trading activities.

($0 commissions on online listed stock, Source: Schwab)

Mutual funds, on the other hand, have a different fee structure. The expense ratio is the most important cost here. It is an annual fee that the fund charges to cover its running costs. According to the Investment Company Institute's report, the average expense ratio for equity mutual funds was 0.42% in 2023. For bond mutual funds, it is 0.37%.

But that's not the whole story. Some mutual funds also charge:

Front-end load: A fee paid when you buy shares (can be up to 5.75%)

Back-end load: A fee paid when you sell shares

12b-1 fees: Annual marketing or distribution fees (up to 1% of your investment)

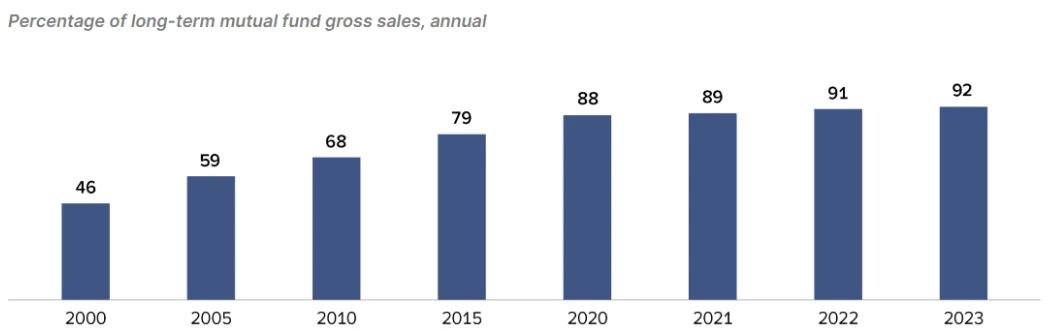

A lot of investors are moving their money to no-load funds. In 2023, 92% of gross sales of long-term mutual funds went to no-load funds without 12b-1 fees, compared to just 46% in 2000.

(Percentage of long-term mutual fund gross sales, annual, Source: ICI.org)

Stocks vs. Mutual Funds: Risk and Return

Stocks generally offer higher potential returns but come with greater risk. According to a study by J.P. Morgan, the S&P 500 (a broad index of U.S. stocks) has delivered an average annual return of about 10% over the long term. However, this comes with significant volatility.

Mutual funds, especially those that are well-diversified, typically offer more moderate returns with lower risk. For example, the Fidelity Blue Chip Growth (FBGRX) fund, which invests in large- and mid-cap growth stocks, had a year-to-date performance of 23.45% as of August 2024 and a 5-year historical performance of 169.7%.

Stocks vs. Mutual Funds: Tax Implications

Let's break down how these two popular investment options are taxed in the U.S.

Capital Gains Tax

For both stocks and mutual funds, you'll pay capital gains tax when you sell your investment for a profit. The tax rate depends on how long you've held the investment:

Short-term capital gains (held for one year or less): Taxed as ordinary income, with rates up to 37% in 2024.

Long-term capital gains (held for more than one year): Taxed at 0%, 15%, or 20%, depending on your income.

Dividend Taxation

Stocks and mutual funds can both pay dividends, but there's a key difference:

Individual stocks: Dividends are taxed when you receive them, even if you reinvest.

Mutual funds: Dividends are taxed when the fund distributes them, which can happen even if you haven't sold any shares.

Qualified dividends are taxed at the same rates as long-term capital gains, while non-qualified dividends are taxed as ordinary income.

Mutual Fund Distributions

Mutual funds have an additional tax consideration: capital gains distributions. These occur when the fund manager sells securities within the fund for a profit. Even if you haven't sold any shares, you'll owe taxes on these distributions.

Stocks vs. Mutual Funds: Pros and Cons

Investment Type | Pros | Cons |

Stocks | • Higher potential returns • Ownership in real companies • High liquidity • Potential dividend income • Compounding growth potential | • High volatility • Risk of significant losses • Requires more time and knowledge • Emotional stress from market fluctuations • Individual stock risk |

Mutual Funds | • Professional management • Instant diversification • Lower risk due to diversification • Potentially steadier returns • Less emotional stress | • Management fees and expenses • Less control over specific investments • Potential for lower returns than individual stocks • Tax implications from fund distributions • Minimum investment requirements |

Wrapping Up: Which is Better - Stocks or Mutual Funds?

Investing in stocks or mutual funds depends on your personal financial situation, your long-term goals, and your risk tolerance.

Stocks might be better for:

Investors comfortable with higher risk and market volatility

Those with time to research and monitor individual companies

People seeking potentially higher returns and don't mind short-term fluctuations

Mutual funds could be the right choice for:

Beginners or those with limited time for investment research

Investors seeking professional management and diversification

People who prefer a more hands-off approach to investing

Many successful investors use a combination of both stocks and mutual funds in their portfolios. This approach can help balance the potential for high returns with the benefits of diversification and professional management.

The "better" choice is the one that fits with your personal financial plan and lets you sleep well at night. Consider consulting with a financial advisor to find the best mix for your specific needs.