What is Retirement Planning? A Complete Beginner’s Guide

Dany M.

What is a Retirement Plan?

A retirement plan is a financial strategy that outlines how you will save and invest your money to ensure a comfortable and secure life after you stop working. It takes into account your current financial situation, future income sources, estimated expenses, and desired lifestyle in retirement. It's like a roadmap to a comfortable and secure future.

For example, when you retire, you'll probably want to enjoy your life without worrying about money. You might want to travel, spend time with family, or pursue hobbies. But to do all those things, you'll need a steady income even when you're not working anymore.

What is Retirement Planning?

Retirement planning is the process of creating and implementing your retirement plan. It involves setting retirement income goals, determining the steps needed to achieve those goals, and making smart decisions about saving, investing, and managing potential risks along the way.

What Retirement Looks Like in America Today?

Many Americans are struggling to save enough for retirement and facing the prospect of delayed retirement. However, there is also a growing awareness of the importance of retirement planning and a willingness to embrace new possibilities for retirement life.

Over 12,000 Americans will turn 65 every day in 2024. (Yahoo)

In 2024, the average retirement age is 64.7 for men and 62.1 for women, up from just 57 in 1991. (Zippia)

56% of Americans say they're behind on saving for retirement. (Bankrate)

58 million working-age Americans have no retirement savings at all. (BenefitsPRO)

Nearly 7 in 10 Americans between ages 50 and 74 don't have a formal retirement plan, and 88% of people believe the generation after theirs will have a more difficult time retiring than they did. (Magnify Money)

Almost half of Americans between the ages of 60-75 say they plan to work part-time in retirement. (Forbes)

On average, Americans believe they'll need $1.8 million to retire comfortably. However, only 37% of workers believe they'll be able to achieve this goal. (USA Today)

67% of people said their employer offered a 401(k) or similar employer-sponsored plan, and 77% of those individuals chose to participate. (FA Mag)

Current Retirees Are Facing Challenges

44% of retirees struggle to afford basic living expenses. (Clever)

71% of retirees carry debt through their retirement. (Yahoo)

41% of Baby Boomers say Social Security will be their primary source of income in retirement. (The Motley Fool)

48% of retirees believe they'll outlive their savings, and 37% have no retirement savings left. (Clever)

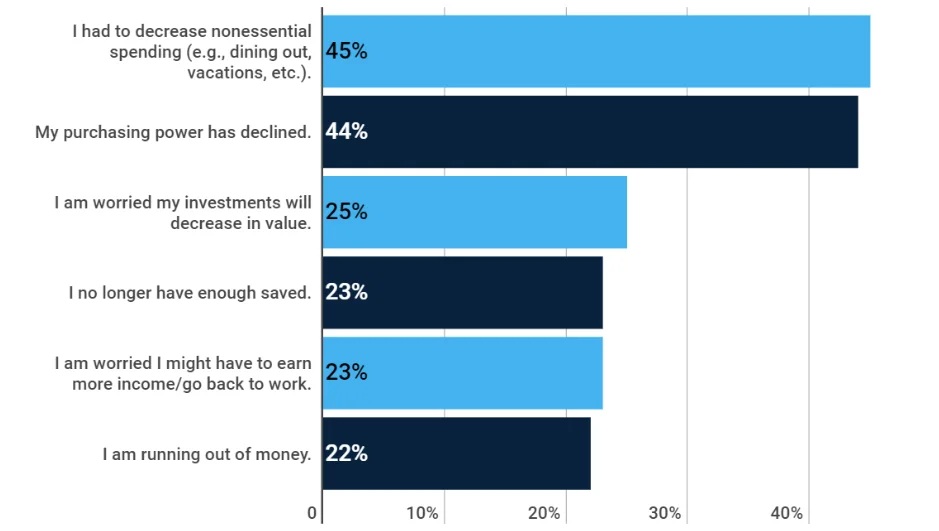

Current retirees are also being affected by inflation, they say:

(How Inflation is Impacting US Retirees, Source: Clever)

40% of older Americans said they're delaying retirement due to inflation, and 22% of working Americans are likely to retire in 2024. (BenefitsPRO)

In summary, retirement in America looks like this:

Insufficient savings, especially among younger generations

Heavy reliance on Social Security, which faces long-term funding challenges

A large wave of Baby Boomers is retiring, but some are choosing to keep working

Younger generations are facing more uncertainty and obstacles to achieving retirement security

A notable gender gap in retirement preparedness and confidence

The traditional notion of retirement is changing, with many needing to work longer, having less guaranteed income, and facing more complex financial challenges than previous generations. Effective planning and saving are more critical than ever to secure a comfortable retirement in this environment.

How Can You Define Your Ideal Retirement Lifestyle?

Your retirement lifestyle will largely depend on your personal preferences and goals. Some people dream of traveling the world, while others may prefer a quiet life close to family and friends. Take the time to envision your ideal retirement lifestyle and consider factors such as:

Where you want to live (staying in your current home, downsizing, or relocating)

How you want to spend your time (hobbies, volunteering, part-time work)

What experiences do you want to have (travel, learning new skills, pursuing passions)

What Expenses Should You Consider in Retirement?

Once you know what you want, estimate the expenses associated with your desired retirement lifestyle. Consider both your basic living expenses (housing, food, healthcare) and discretionary expenses (travel, entertainment, hobbies).

Keep in mind that your expenses may change over time, especially as you age and your healthcare needs increase. It's important to factor in inflation and potential long-term care costs when estimating your retirement expenses.

How Much Should You Aim to Save for Retirement?

With a clear understanding of your retirement lifestyle and estimated expenses, you can calculate how much you'll need to save to achieve your goals. A common rule of thumb is to aim for a retirement nest egg of 25 times your annual expenses.

For example, if you estimate your annual retirement expenses to be $50,000, you'll need a savings goal of $1.25 million ($50,000 x 25).

However, this is a general guideline, and your specific savings goal will depend on factors such as:

Your expected retirement age

Your estimated life expectancy

Your investment returns

Your sources of retirement income (Social Security, pensions, part-time work)

Consider using online retirement calculators and tools or consulting with a financial advisor to get a more personalized estimate of your retirement savings needs.

Life Stages For Retirement Planning

Each stage of life brings with it unique financial priorities, challenges, and opportunities. Understanding these stages can help you put together a more effective and personalized retirement plan.

A. Early career (20s-30s)

When you're in your 20s and 30s, retirement might feel like it's a long way off, but this is actually the perfect time to start building a strong financial foundation. If your employer offers a retirement plan like a 401(k) or 403(b), it's a smart idea to sign up, especially if they offer to match some of the money you put in. If you don't have a plan at work, think about opening an Individual Retirement Account (IRA) and try to put in as much as you can each year.

It's also important to develop good money habits during this time, like making a budget, saving regularly, and paying off debt from credit cards and student loans. By starting early and saving consistently, you can take advantage of compound interest, which helps your retirement savings grow over time.

B. Mid-career (40s-50s)

When you reach your 40s and 50s, you're likely earning more money, so it's a good time to really focus on saving for retirement. Try to put as much as possible into your workplace retirement plan and think about opening additional investment accounts like a Roth IRA or a regular brokerage account.

This is also a good time to take another look at your investment strategy and make sure you have a mix of different types of investments. Consider working with a financial advisor to create an investment plan that matches your comfort with risk and your retirement goals.

Additionally, start thinking about expenses you might have in retirement, like healthcare and long-term care. Look into buying long-term care insurance or opening a Health Savings Account (HSA) if you have a high-deductible health plan.

C. Pre-retirement (50s-60s)

As retirement gets closer, it's important to fine-tune your plan and make sure you're on the right track. Use online retirement calculators or talk to a financial advisor to see if you're saving enough to reach your retirement goals. If you're falling behind, take advantage of catch-up contributions in your 401(k) and IRA, which let you save extra money once you turn 50.

This is also the time to start thinking about when to claim Social Security benefits. While you can start collecting as early as age 62, waiting until your full retirement age (66-67, depending on when you were born) or even later can make your monthly payments significantly bigger.

Think about your health, how long you expect to live, and your overall financial situation when deciding on the best time to start claiming benefits.

D. Retirement years

Once you've retired, your focus changes from saving money to managing the money you have and your expenses. Make a detailed retirement budget based on the money you expect to have coming in (Social Security, pension, money from retirement accounts) and the expenses you think you'll have.

Figure out a withdrawal rate from your retirement accounts that you can stick with to make sure your savings last throughout your retirement. The traditional 4% rule (taking out 4% of your portfolio in the first year of retirement and adjusting for inflation each year after) is a good place to start, but you may need to adjust based on your specific situation.

How to Build Your Retirement Plan

Creating a solid retirement plan involves several key components that work together to help you achieve your goals and enjoy a financially secure future. Let's take a closer look at these essential elements and how they fit into your overall retirement strategy.

A. Savings Strategies

At the heart of any successful retirement plan is a commitment to consistent saving. Start by setting aside a portion of your income each month, aiming to save at least 10-15% of your pre-tax earnings. If that feels like a stretch, don't worry – start with a smaller percentage and gradually increase it over time. The important thing is to make saving a habit and stick with it for the long haul.

One easy way to stay on track is to automate your savings. Set up direct deposits from your paycheck into your retirement accounts, so you don't have to think about it each month. And if your employer offers a 401(k) with matching contributions, be sure to take full advantage of that.

B. Investment planning

Saving is important, but it's only part of the equation. To really make your money work for you, you'll need to invest it wisely. That means creating a diversified portfolio that includes a mix of stocks, bonds, and cash equivalents according to your age, risk tolerance, and retirement timeline.

Regularly rebalance your portfolio to maintain your desired asset allocation. Consider investing in low-cost index funds and exchange-traded funds (ETFs) to minimize fees and maximize returns.

Additionally, consider incorporating other sources of income such as rental properties, part-time work, or annuities to supplement your Social Security and pension benefits. By creating multiple income streams, you can increase your financial stability and reduce the risk of outliving your savings.

If you're not sure where to start, consider working with a financial advisor. They can help you develop a personalized investment strategy and make informed decisions based on your unique needs and goals.

C. Tax considerations

Optimizing your tax strategy can help you keep more of your hard-earned money in retirement. When considering retirement accounts, it's important to understand the tax implications of traditional and Roth options.

Traditional 401(k)s and IRAs offer upfront tax deductions on your contributions, which can help lower your current tax bill. However, you'll need to pay taxes on withdrawals in retirement. For 2024, contribution limits are:

401(k)s: $23,000 ($30,500 if you're 50 or older)

IRAs: $7,000 ($8,000 if you're 50 or older)

Roth accounts, on the other hand, don't provide immediate tax benefits but offer tax-free withdrawals in retirement, including earnings, if certain conditions are met. This can be advantageous if you expect to be in a higher tax bracket in retirement. Additionally, Roth IRAs offer:

Tax-free growth

No required minimum distributions (RMDs)

The ability to pass money to heirs tax-free

The choice between traditional and Roth accounts depends on your current tax situation, expected future tax rates, and overall financial goals. It's worth noting that:

Traditional IRA deductions may be limited based on income and access to employer-sponsored plans

Roth IRA contributions have income limits

One smart strategy is to diversify your tax exposure by contributing to a mix of pre-tax and after-tax accounts. That way, you'll have more flexibility and control over your tax situation in retirement.

D. Insurance and healthcare planning

Healthcare costs can be a big expense in retirement. Even with Medicare, you'll likely have out-of-pocket costs for things like deductibles, copays, and prescription drugs. That's why it's important to factor healthcare into your overall retirement plan.

Consider purchasing supplemental insurance, like a Medigap policy or a Medicare Advantage plan, to help cover some of those extra costs. And don't forget about long-term care insurance – it can be a lifesaver if you ever need extended care services like assisted living or in-home care.

Of course, insurance isn't just about healthcare. Make sure you have adequate life insurance and disability coverage to protect your income and provide for your loved ones in case something unexpected happens.

E. Estate planning

No one likes to think about death, but having a solid estate plan in place can give you peace of mind, knowing that your wishes will be carried out and your loved ones will be taken care of. That means having a will that specifies how you want your assets distributed, as well as powers of attorney that designate someone to make financial and healthcare decisions on your behalf if you become incapacitated.

You may also want to consider setting up trusts, which can help minimize estate taxes and give you more control over how your assets are distributed.

Regularly review and update your beneficiary designations on retirement accounts, life insurance policies, and other assets to ensure they align with your overall estate plan.

F. Housing considerations

For many people, housing is the biggest expense in retirement. So, it's important to think carefully about where you want to live and how it fits into your overall retirement plan.

Some people choose to downsize to a smaller home or move to an area with a lower cost of living. Others prefer the convenience and amenities of a retirement community or assisted living facility. And some people want to stay put in their current home, but may need to make modifications to accommodate aging in place.

Whatever you decide, be sure to factor the costs into your retirement budget. That includes things like mortgage or rent payments, property taxes, maintenance and repairs, and any necessary renovations or upgrades. And don't forget about the possibility of using your home equity as a source of income in retirement through options like a reverse mortgage.

When Should You Retire?

The right retirement age depends on your unique situation. You should consider the following factors:

1. Financial readiness

Make sure you have enough savings and income to support your desired retirement lifestyle. Take a close look at your expenses, including healthcare costs, and compare them to your expected income from Social Security, pensions, and personal savings.

2. Health and life expectancy

Your health can influence your retirement timing. If you're healthy and expect to live long, working longer can help your savings last. If you have health concerns, retiring earlier might be better.

3. Personal goals

Think about what you want to do in retirement, like traveling, hobbies, or spending time with family. Your retirement timing should match your aspirations and values.

4. Job satisfaction

If you love your work, you might keep working longer. If you're burnt out or ready for a change, retirement could be a welcome shift.

How Does Your Retirement Age Affect Your Finances?

Your retirement age can significantly impact your finances:

Social Security: Starting benefits at 62 means a permanent reduction while waiting until full retirement age (66-67) or later (up to 70) results in higher monthly payments.

Retirement accounts: Retiring before 59½ can trigger early withdrawal penalties on 401(k)s and IRAs. Delaying retirement lets your investments grow more.

Healthcare: Medicare eligibility starts at 65. Retiring earlier means budgeting for alternative health insurance.

According to the 2024 EBRI survey, the median expected retirement age among workers is 65, while the median actual retirement age among retirees is 62.

If you're considering early retirement, plan carefully to ensure your savings last:

Get your savings rate up before you retire

Make a realistic budget that accounts for everything

For extra income, explore part-time work, consulting, or starting a business

Work with a financial advisor to develop a sustainable withdrawal strategy

Common Retirement Planning Mistakes to Avoid

Retirement planning can be complex, and it's easy to make mistakes along the way. Here are some common pitfalls to watch out for:

Starting too late: The earlier you start saving, the more time your money has to grow. Aim to begin saving in your 20s or 30s.

Not saving enough: Experts recommend saving 10-15% of your income for retirement. If you can't save that much right away, gradually increase your contributions over time.

Underestimating expenses: Many people underestimate how much they'll need in retirement. Be sure to account for healthcare costs, which can be significant.

Relying too heavily on Social Security: Social Security is only designed to replace about 40% of your pre-retirement income. You'll need other sources of income to make up the difference.

Not diversifying investments: Putting all your eggs in one basket can be risky. Diversify your portfolio with a mix of stocks, bonds, and other investments.

Failing to plan for long-term care: 70% of Americans over 65 will need some form of long-term care. Consider long-term care insurance to help cover these costs.

Not updating your plan: Life changes, and so should your retirement plan. Review and adjust your plan regularly, especially after major life events.

Wrapping Up

Retirement planning is a marathon, not a sprint. If you take a proactive, long-term approach and avoid common mistakes, you'll reach your retirement goals and enjoy the retirement lifestyle you have always dreamed of.

So, take action today. Start by assessing your current financial situation, setting clear retirement goals, and creating a plan to achieve them. Whether you're just starting your career or nearing retirement age, it's never too early or too late to start planning for your future.