36% of Americans say real estate is the best long-term investment among stocks, savings accounts, and gold.

For pretty obvious reasons, real estate investing has long been a popular way to build wealth and generate passive income. The property has the potential for capital appreciation, regular cash flow from rental income, diversification, and tax benefits.

We’ll explore everything you need to know about real estate investing and how you can start it easily.

What is Real Estate Investing?

At its core, real estate investing involves purchasing, owning, managing, renting, or selling property for profit.

Real estate investments come in many forms, from residential properties like single-family homes and apartments to commercial properties such as office buildings, retail spaces, and warehouses. Even undeveloped land can be a real estate investment.

One of the key attractions of real estate investing is its potential for generating multiple income streams. It can provide both steady income through rent and long-term appreciation in value.

Real estate also offers a hedge against inflation. As the cost of living rises, so do property values and rental rates. This means your investment is likely to keep pace with or even outpace inflation, protecting your purchasing power over time.

How Can You Start Investing in Real Estate?

Whether you come with big money up front or not so much, there is a way to invest in real estate. Each strategy has its own advantages and disadvantages, so the key is to find one that meets your financial goals and attitude toward risk. Here are some common investment options in real estate:

1. Buy and Hold

The buy-and-hold strategy is perhaps the most straightforward approach to real estate investing. It involves purchasing a property and holding onto it for an extended period, typically years or even decades. The goal is to benefit from long-term appreciation while potentially earning rental income along the way.

According to the Federal Reserve Bank of St. Louis, the average sales price of houses sold in the United States has seen substantial growth over the decades, with various periods showing an average annual increase of around 4% to 5%.

How to Invest

To implement this strategy, you'll need to do your homework. Start by researching areas with potential for long-term growth. Look at factors like job market trends, population growth, and planned developments.

Once you've identified a promising location, you'll need to secure financing. Investment properties typically require a down payment of 20-25%, so be prepared for a significant upfront investment.

Pros

Potential for significant appreciation over time

Steady rental income if you lease the property

Tax benefits, including deductions for mortgage interest and property taxes

Building equity as you pay down the mortgage

Cons

Requires substantial upfront capital

Property may not appreciate as expected

Ongoing costs for maintenance and property taxes

Less liquid than other investments

2. Become a Landlord (Rental Properties)

You can also invest in rental properties. In this case, you buy a residential or commercial property and lease it to tenants. It's a way to earn regular monthly income while still getting the benefit of property appreciation. Approximately 44.1 million American households are renters, indicating a strong demand for rental properties.

How to Invest

To get started as a landlord, you'll first need to identify a suitable property in a desirable rental area. Financing for rental properties often requires a higher down payment than owner-occupied homes, typically around 25-30%.

As soon as you've got the property, you'll have to prepare it for tenants, which may include renovations and upgrades. You can manage the property yourself or hire a property management company.

Pros

Regular monthly income from rent

Potential for property appreciation

Tax deductions for property-related expenses

Building equity while tenants pay down your mortgage

Cons

Dealing with tenant issues and property maintenance

Potential for vacancies and loss of income

Property damage risks

Time-consuming if self-managed

3. House Flipping

For those seeking a more hands-on and potentially quicker return on investment, house flipping can be an exciting option. This strategy involves purchasing undervalued properties, renovating them, and selling them quickly for a profit.

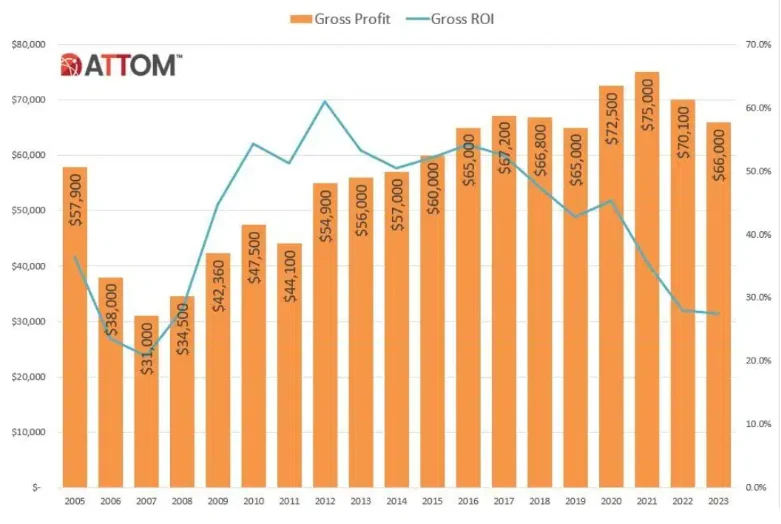

The potential returns from house flipping can be substantial. According to ATTOM Data Solutions, house flippers averaged a gross profit of $66,000 per flip in 2023, representing a 27.5% return on investment.

(U.S. Home Flipping Gross Profit & Returns, source: ATTOM)

In the same year, 308,922 single-family homes and condos were flipped, accounting for about 8.1% of all home sales.

How to Invest

Successful house flipping requires a keen eye for undervalued properties and the ability to estimate renovation costs accurately. You'll need to research local markets thoroughly to find properties with potential. Financing for flips often comes through hard money loans or cash, as traditional mortgages can be challenging to secure for short-term investments.

Pros

Potential for quick, high returns

Opportunity to add significant value through renovations

Shorter-term investment compared to buy-and-hold

Develops your real estate and renovation expertise

Cons

Requires significant time, effort, and expertise

Risk of unexpected renovation costs

Market changes can affect profitability

Potential for properties to sit unsold, incurring holding costs

4. Real Estate Investment Groups (REIGs)

For those who want to invest in real estate but prefer a more hands-off approach, Real Estate Investment Groups (REIGs) can be an attractive option. REIGs are like small mutual funds for rental properties, allowing you to own one or more units in a larger property or development.

How to Invest

To invest in a REIG, you'll typically need to meet a minimum investment requirement and may need to pay ongoing fees. In return, you'll receive a share of the income and appreciation based on your investment. The group handles the management of the properties, including finding tenants, handling maintenance, and dealing with vacancies.

Pros

More hands-off than direct property ownership

Allows for diversification across multiple properties

Professional management handles tenant and maintenance issues

Can start with a smaller investment compared to buying whole properties

Cons

Less control over investment decisions

Ongoing fees can eat into returns

Dependent on the group's management quality

May have less liquidity than other real estate investments

5. Commercial Real Estate

You can diversify beyond residential properties by investing in commercial real estate, which includes office buildings, retail spaces, warehouses, and other business properties.

Commercial real estate is a big market. The total global commercial real estate investment volume in 2023 was $647 billion (which is down from $1.14 trillion in 2022).

(Commercial Real Estate Investment Dollar Volume, Source: CBRE)

However, CBRE predicts that investment activity will recover in the second half of 2024 due to stabilizing market conditions, central banks cutting interest rates, and positive economic forecasts.

How to Invest

Investing in commercial real estate often requires a larger capital investment than residential properties, with down payments typically ranging from 30-35%. You can invest directly by purchasing properties or indirectly through commercial real estate funds.

Pros

Potentially higher returns than residential real estate

Longer lease terms, often with built-in rent escalations

Triple net leases can pass property expenses to tenants

Diversification from residential real estate market

Cons

Requires larger capital investment

More complex management and leasing processes

Vulnerable to economic downturns

May require specialized knowledge of business sectors

6. Real Estate Crowdfunding Platforms

One of the most revolutionary changes in real estate investing is the rise of crowdfunding platforms. These online platforms allow investors to pool their money with others to invest in properties they might not be able to afford individually. Companies like Fundrise, RealtyMogul, and CrowdStreet have made it possible for individuals to invest in commercial and residential real estate with as little as $500.

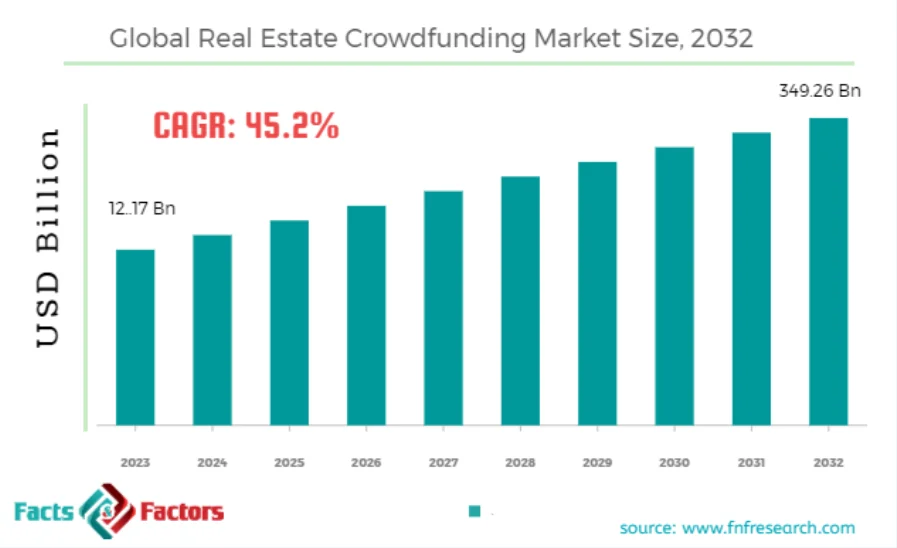

According to a report by Facts & Factors, the global real estate crowdfunding market is expected to reach $849.26 billion by 2032, growing at a CAGR of 45.2% from 2024 to 2032.

(Global Real Estate Crowdfunding Market Size, Source: Facts & Factors)

This explosive growth reflects the increasing popularity and accessibility of this investment method.

How to Invest

To get started with real estate crowdfunding, you'll first want to research popular platforms like Fundrise, RealtyMogul, or CrowdStreet. Each of these platforms has its own focus and minimum investment requirements, so take the time to find one that aligns with your investment goals and budget. Once you've chosen a platform, you'll need to create an account and verify your identity.

After setting up your account, you can browse through available investment opportunities. You'll typically find a mix of residential, commercial, and mixed-use properties. It's crucial to conduct thorough due diligence at this stage.

Carefully read the offering documents, paying close attention to projected returns, risk factors, and fee structures. When you're ready to invest, you can often start with as little as $500, making this an accessible option for many beginners.

Pros

Low minimum investments

Access to commercial-grade properties

Diversification across multiple properties

Passive income potential

Cons

Investments are often illiquid

Limited control over investment decisions

Potential for platform failure

Fees can eat into returns

7. Real Estate Investment Trusts (REITs)

While not entirely new, REITs have evolved to become more accessible to average investors. These companies own, operate, or finance income-producing real estate across various sectors. Publicly traded REITs offer high liquidity and can be bought and sold like stocks, making them an attractive option for those who want real estate exposure without directly owning property.

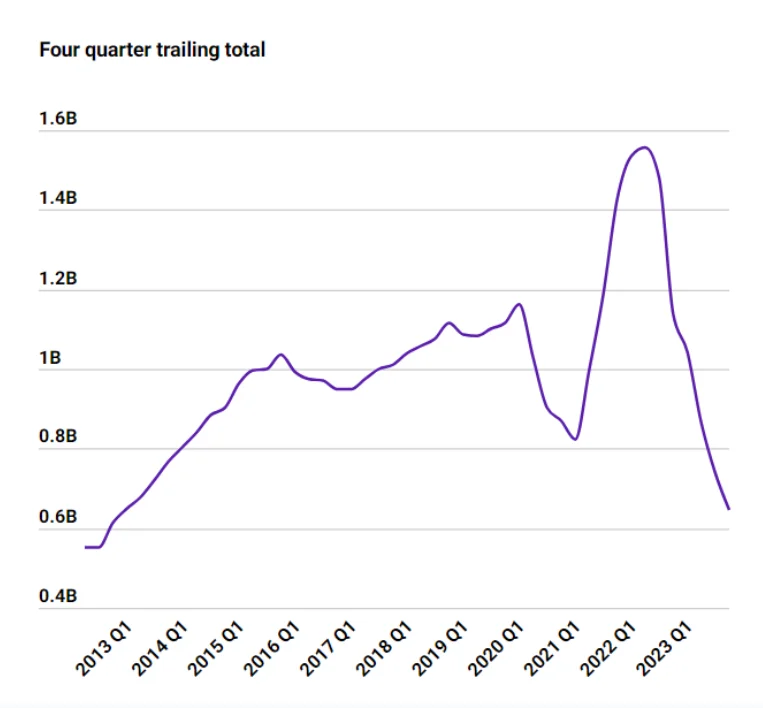

In 2023, the total market capitalization of publicly traded REITs in the U.S. was approximately $1.37 trillion, according to Statista.

.webp)

(The market capitalization of real estate investment trusts (REITs) in the United States, Source: Statista)

This figure highlights just how important REITs are in modern real estate investing.

How to Invest

Investing in REITs is relatively straightforward. If you don't already have one, you'll need to open an account with a brokerage firm. Popular options include Fidelity, Charles Schwab, or Robinhood. Once your account is set up, you can start researching different types of REITs. There are REITs focusing on various property types, including residential, commercial, healthcare, and more.

When analyzing REITs, it's important to look at metrics like funds from operations (FFO), dividend yield, and price-to-FFO ratio. These can give you insights into the REIT's performance and valuation. Once you've chosen a REIT, you can purchase shares through your brokerage account, just like you would with stocks.

Pros

High liquidity for publicly traded REITs

Professional management

Diversification across multiple properties

Regular dividend income

Cons

Sensitive to interest rate changes

Potential for high fees in some private REITs

Less control over specific property investments

Dividends are taxed as ordinary income

8. Real Estate Tokenization

Blockchain technology has paved the way for real estate tokenization, where property ownership is divided into digital tokens. This method allows for fractional ownership of high-value properties, increasing accessibility and liquidity in the real estate market. Platforms like RealT and Blocksquare are pioneering this space, offering tokenized real estate investments to a global audience.

While still in its early stages, the potential for growth is significant. The global real estate tokenization market is expected to hit $4.22 billion by 2027, with a solid growth rate of 28.3% every year.

How to Invest

To invest in tokenized real estate, you'll typically need to set up a digital wallet to hold your tokens. Most platforms also require Know Your Customer (KYC) verification to comply with financial regulations.

Once your account is set up, you can browse available tokenized properties on the platform. When you find a property you're interested in, you can purchase tokens representing fractional ownership in that property.

Pros

Fractional ownership of high-value properties

Increased liquidity compared to traditional real estate

Global access to real estate markets

Transparent transactions through blockchain

Cons

Regulatory uncertainty in some jurisdictions

Technology risks associated with blockchain

Limited track record for many platforms

Potential for high volatility in token prices

9. Real Estate Debt Investing

Real estate debt investing is another option for investors, especially those looking to enter the real estate market without directly owning properties. This involves lending money to real estate projects or investing in mortgage-backed securities.

How to Invest

To get started with real estate debt investing, you'll want to explore platforms like PeerStreet, Groundfloor, or RealtyMogul. These online marketplaces connect investors with real estate developers and property owners seeking loans.

After creating an account and completing the necessary verification processes, you'll be able to browse through a variety of loan opportunities.

When evaluating potential investments, you'll need to consider factors such as interest rates, loan-to-value ratios, and loan terms.

Pros

Regular income streams

Lower risk compared to equity investments

Shorter investment horizons

Potential for higher yields than traditional fixed-income investments

Cons

Risk of borrower default

Sensitive to interest rate changes

Less potential for capital appreciation

Complex to evaluate for individual investors

10. House Hacking

A modern twist on traditional real estate investing, house hacking involves purchasing a multi-unit property, living in one unit, and renting out the others. This strategy allows investors to offset their mortgage and living expenses with rental income. While not a new concept, its popularity has surged among millennials and first-time homebuyers looking to enter the real estate market.

Mynd says that 43% of millennials and Gen Z are choosing to become "rentvestors" – renting where they live while owning investment properties elsewhere.

How to Invest

You'll first need to research areas with strong rental markets and affordable multi-unit properties. Look for neighborhoods where rental demand is high, and property prices are within your budget. Once you've identified potential areas, it's time to get pre-approved for a mortgage. Many house hackers opt for FHA loans, which allow for lower down payments, making it easier to get started.

When searching for a suitable property, consider options like duplexes, triplexes, or houses with extra rooms that can be rented out. The aim should be finding a property where the potential rental income from the other units or rooms can cover a significant portion of your mortgage payment and other housing expenses.

Pros

Live for free or at a reduced cost

Build equity while others pay your mortgage

Qualify for owner-occupied financing

Cons

Living close to tenants can be challenging

Responsible for property management and maintenance

Potential for difficult tenants

May limit personal space and privacy

What Are the Tax Implications of Real Estate Investing?

Understanding tax implications is important, especially for seasoned investors who may want to learn which strategies could offer them potential benefits and keep themselves in line with current laws.

Here are the most important tax aspects you must know for real estate investors in the U.S. as of 2024:

Capital Gains Tax

When you sell an investment property for a profit, you'll be subject to capital gains tax. The rate depends on how long you've held the property:

Short-term capital gains (property held for one year or less): Taxed as ordinary income, with rates ranging from 10% to 37%, depending on your tax bracket.

Long-term capital gains (property held for more than one year): Taxed at preferential rates of 0%, 15%, or 20%, based on your taxable income.

For 2024, the long-term capital gains tax brackets are:

0% for single filers with taxable income up to $47,025 and married couples filing jointly with taxable income up to $94,050.

15% for single filers with taxable income between $47,026 and $518,900, and married couples filing jointly with taxable income between $94,051 and $583,750.

20% for single filers with taxable income over $518,900 and married couples filing jointly with taxable income over $583,750.

It's worth noting that an additional 3.8% Net Investment Income Tax (NIIT) may apply to individuals with modified adjusted gross income exceeding $200,000 ($250,000 for married couples filing jointly).

Depreciation Deduction

The IRS allows you to deduct the cost of your investment property over its useful life, a concept known as depreciation. For residential properties, the depreciation period is 27.5 years, while for commercial properties, it's 39 years. This deduction can significantly reduce your taxable rental income.

However, be aware of depreciation recapture when you sell the property. You'll need to pay a 25% tax on the amount you've depreciated over the years, unless you perform a 1031 exchange.

1031 Exchange

A 1031 exchange allows you to defer paying capital gains taxes by reinvesting the proceeds from the sale of one investment property into another "like-kind" property. This can be a powerful tool for growing your real estate portfolio while deferring tax liabilities.

Rental Income and Deductions

Rental income is taxable, but you can deduct various expenses associated with your rental property, including:

Mortgage interest

Property taxes

Insurance premiums

Maintenance and repairs

Property management fees

Utilities (if paid by the landlord)

Travel expenses related to property management

These deductions can significantly reduce your taxable rental income.

Passive Activity Loss Rules

Real estate investing is generally considered a passive activity by the IRS. If your rental properties operate at a loss, you may only be able to deduct up to $25,000 of those losses against your other income, and this deduction phases out for higher-income earners. Unused losses can be carried forward to future tax years.

However, if you qualify as a real estate professional (by spending more than 750 hours per year in real estate activities), you may be able to deduct these losses without limitation.

Opportunity Zones

Investing in designated Opportunity Zones offers significant tax benefits, including:

Deferral of capital gains taxes on investments rolled into Opportunity Funds until December 31, 2026

Reduction of the tax you'll owe by up to 15% after 7 years

Potential elimination of taxes on gains from the Opportunity Fund investment if held for at least 10 years

Self-Employment Tax

If you're actively involved in managing your properties or flipping houses, you may be subject to self-employment tax (15.3% as of 2024) on your real estate income. However, rental income is typically not subject to self-employment tax unless you're providing substantial services to tenants. The specific rules can be complex and depend on various factors. It's always best to consult with a tax professional for individual situations.

What Common Mistakes Should New Real Estate Investors Avoid?

Real estate investing can be a great way to build wealth, but it does come with its challenges. If you're a new investor, being aware of common mistakes can really help you navigate the market more smoothly. Here are some key errors to avoid:

Lack of Planning - Diving in without a clear strategy can lead to poor investment choices. Develop a comprehensive plan outlining your goals and preferred property types.

Underestimating Costs - Don't focus solely on purchase price. Account for closing costs, taxes, insurance, maintenance, and potential vacancies.

Neglecting Due Diligence - Always thoroughly research the property, local market, and potential legal issues before investing.

Ignoring Location - Remember, you can change a property, but not its location. Consider factors like neighborhood quality and proximity to amenities.

Emotional Decision Making - Base your investments on numbers and facts, not emotions or fear of missing out.

Inadequate Financing Knowledge - Understand different mortgage options for investment properties to structure deals effectively.

Poor Tenant Screening - For rentals, thorough tenant screening is crucial to avoid costly problems down the line.

Overlooking Market Cycles - Be aware of real estate market trends to avoid overpaying during market peaks.

Trying to Do Everything Alone - Build a team of professionals, including a real estate agent, attorney, and accountant, to navigate complex situations.

Underestimating Time Commitment - Be prepared for the time investment required, especially if managing properties yourself.

Wrapping Up

Every successful real estate investor started somewhere. Real estate investing offers multiple strategies for wealth creation, but it isn't a guaranteed path to riches. It requires careful research, strategic planning, and often a significant upfront investment.

Like any investment, it comes with risks, including market fluctuations, property damage, and the potential for problematic tenants. Consider starting small with a single-family home to gain experience. Always do your homework on potential deals and connect with other investors to share insights.

Remember, real estate is a long-term game, so be patient and stay committed to learning and growing.

Stay connected with us for more tips and guides on investing!