Real Estate vs. Stocks: Which One is the Better Investment?

Dany M.

For investors seeking to grow their wealth, real estate and stocks are major options. In fact, 36% of Americans identify real estate as their top long-term investment choice, and 22% favor stocks and mutual funds. Although both of these investment strategies can offer good returns, they are different in how they work, the risks they involve, and the rewards they offer.

But which option is truly better? The answer isn't one-size-fits-all. Investors need to know the difference between stocks and real estate in order to make choices that will help them reach their overall financial goals.

Real Estate vs. Stocks: What Options Do Investors Have?

Investors can make money in different ways with stocks and real estate. These two main groups give investors many sub-options to choose from. The choice between real estate and stocks depends on an investor's financial goals, risk tolerance, and investment timeline. The good news is that you do not have to choose between the two; many investors include a small amount of each in their portfolios.

Real Estate Options & Income

Some popular types of real estate investments are single-family homes, multi-family homes, commercial property, and real estate investment trusts (REITs).

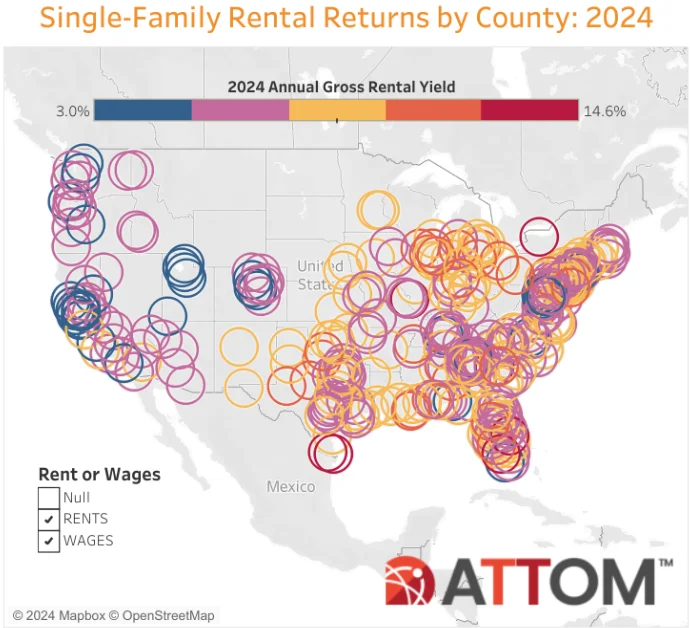

With real estate, you can earn rental income by leasing out properties to tenants. A study by ATTOM Data Solutions says that in 2024, the average annual gross rental yield for a three-bedroom home will be 7.55 percent. This is calculated by dividing the annualized gross rent income by the median purchase price. The study looked at 341 counties.

(Single-Family Rentals Returns by County in 2024, Source: ATTOM)

See an interactive map showing the SFR returns for each of the 341 counties that were examined.

But that's not the only way to make money from real estate. Real estate can also provide income through appreciation when the property's value increases over time. The Federal Reserve Bank of St. Louis says that the median sales price of homes sold in the U.S. in the second quarter of 2024 was $412,300. This is a big jump from the previous few years.

Stock Options & Income

Stock investments can be made through individual stocks, mutual funds, exchange-traded funds (ETFs), and index funds.

Stocks generate income primarily through dividends and capital gains. Dividends are payments made by companies to their shareholders, typically on a quarterly basis. These payments represent a portion of the company's profits and can provide a regular income stream. By June 2024, the dividend yield for S&P 500 companies was around 1.32%. However, this is lower than the long-term average of 1.83%.

When a stock is sold for more than it was bought for, the investor makes a capital gain. This can be a significant source of income, especially for growth stocks. For example, if you had invested in Tesla (TSLA) stock in January 2016, your investment would have increased by approximately 1,500% by now (August 2024).

Real Estate vs. Stocks: Which Has More Risk?

It’s no secret that both real estate and stocks have their fair share of ups and downs, which can have a big effect on investment decisions. Let's break it down and see how they compare.

Real Estate Volatility

Real estate is often seen as a safer investment due to the tangible nature of the assets. Property values typically increase over time, acting as a buffer against inflation. However, changes in the market do affect real estate. Factors such as economic downturns, changes in interest rates, and shifts in supply and demand can impact property values and rental income.

For instance, according to official data from S&P Dow Jones Indices, the S&P CoreLogic Case-Shiller U.S. National Home Price Index fell by approximately 27.4% from its peak in July 2006 to its trough in February 2012.

Additionally, Real estate investments can carry other risks. For example, properties can face issues like natural disasters, unexpected maintenance costs, or changes in local regulations that can impact their value. These risks are often more localized and specific compared to the broader market risks that affect stocks.

Stocks Volatility

Stocks, on the other hand, are known for their higher volatility. The stock market can experience significant swings in short periods, influenced by factors such as company performance, economic indicators, and global events. For example, the S&P 500, a broad market index, experienced a decline of roughly 50% during the Great Recession of 2008-2009.

Real Estate vs. Stocks: Diversification Potential

Diversification within each asset class can help mitigate risk. Let's take a closer look at how each asset class offers opportunities for diversification.

Diversification Potential for Real Estate

Real estate also offers various avenues for diversification, although they may require more capital or effort to implement compared to stocks:

Property types - Investing in residential, commercial, industrial, and retail properties.

Geographic location - Spreading investments across different cities, states, or countries.

Real Estate Investment Trusts (REITs) - Gaining exposure to large-scale, income-producing real estate.

Real estate crowdfunding - Participating in real estate projects with smaller amounts of capital.

Direct vs. indirect investment - Combining property ownership with investments in REITs or real estate funds.

Diversification Potential for Stocks

Stocks provide a wide array of diversification options, making it relatively easy for investors to spread their risk. According to a study by Statman, a well-diversified stock portfolio should contain at least 30-40 different stocks to reduce unsystematic risk significantly.

Stocks provide several avenues for diversification:

Sector diversification - Investing across different industries like technology, healthcare, and finance.

Geographic diversification - Investing in domestic and international markets.

Market capitalization - Combining large-cap, mid-cap, and small-cap stocks.

Investment style - Mixing growth and value stocks.

Dividend stocks - Including stocks that provide regular income.

Stocks vs. Real Estate: Which Is More Liquid?

Stocks are highly liquid investments. You can buy or sell stocks almost instantly during market hours. With online brokers, you can execute trades with just a few clicks. According to a report by the Securities Industry and Financial Markets Association (SIFMA), the average daily trading volume for U.S. equities was about 11 billion shares. This high volume shows you can usually sell your stocks quickly when you need cash.

Real estate, on the other hand, is far less liquid. Selling a property can take weeks, months, or even longer. Properties typically remain on the market for more than 20 days. This doesn't include the time needed for closing, which can add another 30-45 days to the process.

The liquidity difference also affects how quickly you can respond to market changes. With stocks, you can react to news or market shifts almost immediately. If a company reports poor earnings or faces a scandal, you could sell your shares before the price drops significantly. In real estate, you're more locked in. If local property values start to decline, you can't just sell your house in a day.

It is possible to manage liquidity in real estate with the help of Real Estate Investment Trusts (REITs). REITs are companies that own and operate income-producing real estate, and their shares trade on major exchanges, just like stocks. This gives investors a way to invest in real estate with the liquidity of stocks.

Real Estate vs. Stocks: What Are the Costs Associated with Each Investment?

Investing in stocks and real estate has different costs. Let's look at these costs for each.

Real Estate Initial Costs

The most significant upfront cost in real estate is the down payment. According to the National Association of Realtors, the median down payment for first-time homebuyers in 2022 was 6%, while repeat buyers put down a median of 17%. For a $300,000 home, that equates to $18,000 for first-time buyers and $51,000 for repeat buyers.

In addition to the down payment, real estate investors must account for closing costs, which typically range from 2% to 5% of the purchase price. These costs include appraisal fees, title insurance, and mortgage origination fees.

Real Estate Ongoing Costs

Once you own a property, ongoing costs include mortgage payments, property taxes, insurance, and maintenance:

Mortgage Payments: The average monthly mortgage payment in the U.S. was $1,487 in 2022, according to the U.S. Census Bureau.

Property Taxes: Property tax rates and amounts paid vary widely across states and cities. The median property taxes paid for owner-occupied homes can range from $1000 to $9000.

Homeowners Insurance: The average cost of homeowners insurance in the U.S. is $2,270 per year for $300,000 in dwelling coverage. (Source: Bankrate).

Maintenance and Repairs: Experts recommend budgeting 1% to 4% of your home's value annually for maintenance. For a $300,000 home, that's $3,000 to $12,000 per year.

Stock Investment Initial Costs

The initial costs for investing in stocks are much lower. Many online brokers now offer commission-free trading, meaning you can start investing with as little as the price of a single share.

Stock Investment Ongoing Costs

While the upfront costs of investing in stocks are low, there are still ongoing expenses to consider. These include expense ratios for mutual funds and exchange-traded funds (ETFs), which can range from 0.03% to over 1% annually.

If you're working with a financial advisor, you may also pay advisory fees, which typically range from 0.25% to 1% of your assets under management.

In addition to these costs, long-term capital gains tax rates for stocks held over a year are 0%, 15%, or 20%, depending on income.

Real Estate vs. Stocks: How Can Leverage Impact?

Investing in real estate and stocks with leverage and debt can have a huge impact on your profits and risks. Let's look at how each works and the potential benefits and risks.

Leverage in Real Estate

In real estate, leverage typically comes in the form of a mortgage. When you buy a property, you often put down a percentage of the purchase price (known as the down payment) and borrow the rest from a lender. This allows you to control a much larger asset with a smaller initial investment.

For example, if you put 20% down on a $500,000 property, you're controlling a half-million-dollar asset with just $100,000 out of pocket.

The benefit of leverage in real estate is that your return is based on the total value of the property, not just your initial investment. If that $500,000 property appreciates by 10% to $550,000, your $100,000 investment has effectively earned a 50% return (minus interest paid on the mortgage).

Leverage in Stocks

In the stock market, leverage often comes in the form of margin trading. This is when you borrow money from your broker to buy more stock than you could with just your own cash. According to FINRA, you can generally borrow up to 50% of the purchase price of marginable investments.

Like with real estate, margin trading can amplify your returns. If you buy $10,000 worth of stock with $5,000 of your own money and $5,000 borrowed from your broker, a 20% increase in the stock's value would result in a 40% return on your initial investment (minus interest paid on the margin loan).

But just as with real estate, the risk is magnified too. If that same stock declines by 20%, you've lost 40% of your initial investment, plus you still owe your broker the $5,000 you borrowed. Margin rates can also add up.

Real Estate vs. Stocks: What Are the Tax Implications?

Investing in real estate and stocks comes with distinct tax issues that investors must realize in order to maximize their returns.

Real Estate Tax Benefits

Investing in real estate has several tax advantages. One of the most notable is the ability to deduct mortgage interest. According to the IRS, investors can deduct the interest paid on up to $750,000 of mortgage debt used to purchase, build, or improve a rental property.

Property taxes are also deductible, which can help offset the cost of owning rental properties. Additionally, the IRS allows investors to depreciate the cost of residential rental properties over 27.5 years. This depreciation deduction can significantly reduce an investor's taxable income.

When selling a rental property, investors may be able to defer capital gains taxes through a 1031 exchange. This strategy allows investors to reinvest the proceeds from the sale into another similar property without immediately paying taxes on the gains.

Stock Tax Implications

The tax implications of stock investments depend on factors such as the holding period and the type of account used.

Profits from stocks held for less than a year are taxed as ordinary income, up to 37% for the highest earners in 2024.

Profits from stocks held for more than a year are subject to long-term capital gains tax, typically 15% or 20%, depending on income.

Dividends from stocks are also taxable.

Qualified dividends are taxed at the long-term capital gains rate, while non-qualified dividends are taxed as ordinary income.

Regular dividends are taxed as ordinary income, even if they are reinvested, while qualified dividends are taxed at the more favorable capital gains rate.

Investors can minimize taxes on stock investments by using tax-advantaged accounts like 401(k)s or IRAs.

Traditional accounts offer upfront tax deductions, but taxes are paid when funds are withdrawn in retirement.

Roth accounts don't provide an initial tax deduction, but allow for tax-free withdrawals in retirement.

Real Estate vs. Stocks: How Much Control Do You Have?

Your degree of control and management over stocks and real estate investments can vary greatly.

Real Estate

Real estate investing offers the choice between active and passive management:

In active management, investors are fully involved in property selection, tenant screening, rent collection, and maintenance. It offers greater control but requires more time and effort.

In passive management, investors opt for turnkey properties, hire property managers, or invest in REITs. Investors have less direct involvement but also less control.

Stocks

When you invest in stocks, you become a shareholder and a partial owner of the company:

As a shareholder, you have the right to vote on major issues, receive dividends (if declared), and participate in the company's growth.

The level of control depends on the amount of stock owned.

Corporate governance protects shareholders’ interests.

Real Estate: Pros and Cons

Pros | Cons |

1. Potential for steady rental income | 1. High upfront costs (down payments, closing costs, renovations) |

2. Appreciation over time | 2. Time-consuming property management |

3. Tax benefits (mortgage interest, property taxes, depreciation) | 3. Illiquidity compared to other asset classes |

4. Leverage through mortgages can amplify returns | 4. Market volatility based on local economic conditions |

5. Tangible asset with intrinsic value | 5. Ongoing expenses (maintenance, property taxes, insurance) |

6. Hedge against inflation | 6. Potential for problem tenants |

7. Ability to add value through improvements | 7. Geographic limitations and lack of diversification |

8. Passive income potential with property management | 8. Complex legal and regulatory requirements |

9. Opportunity for creative financing strategies | 9. Potential for negative cash flow |

10. Control over investment decisions | 10. Vulnerability to natural disasters and property damage |

Stocks: Pros and Cons

Pros | Cons |

1. Potential for long-term capital growth | 1. Market volatility and risk of loss |

2. Dividend income from some stocks | 2. Requires time and knowledge to invest effectively |

3. High liquidity - easy to buy and sell | 3. Potential tax liability on gains |

4. Low barrier to entry with fractional shares | 4. Short-term fluctuations can cause anxiety |

5. Opportunity for portfolio diversification | 5. No guaranteed returns |

6. Ownership stake in companies | 6. Company-specific risks |

7. Potential for higher returns than savings accounts | 7. Requires ongoing monitoring and research |

8. Access to global markets and industries | 8. Dividends are not guaranteed |

9. Regulated by government agencies (e.g., SEC) | 9. Susceptible to market manipulation |

10. Can align investments with personal values | 10. Emotional decision-making can lead to losses |

Wrapping Up

The choice between real estate and stocks isn't necessarily an either-or decision. Many successful investors incorporate both into their portfolios to balance risk and potential returns.

When considering your investment strategy, remember:

Assess your financial goals, risk tolerance, and time horizon.

Start with thorough research and education about each investment type.

Consider seeking advice from financial professionals.

Begin with a small investment to gain experience before committing larger sums.

Regularly review and rebalance your portfolio to maintain your desired asset allocation.

Ultimately, the best investment strategy is one that aligns with your personal financial goals and risk tolerance.