25 Best Budgeting Tips & Practices (Beginner to Advanced)

Dany M.

People often view budgeting as something they have to do but can't enjoy. However, if you get creative with it, budgeting can be fun and exciting.

It isn't about restricting your life—it's about expanding your possibilities. Whether you're saving for a home or planning for retirement, a budget is your guide to a stress-free life.

With these practical budgeting tips, you can manage your finances with ease and align your spending with your financial goals, so let's get started.

1. Define your "why" for budgeting

Budgeting starts with knowing why you're doing it. Think about your money goals. Do you want to pay off debt? Save for a big purchase? Or maybe build an emergency fund? Having a clear reason helps you stick to your budget when things get tough.

Studies show that people with specific money goals save more. Try making your goal SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of just "save money," you might say, "save $5,000 for a home down payment by December 31st."

Remember, your reason for budgeting is personal. It should match what's important to you and your financial situation.

2. Track every expense for a month

For the next 30 days, write down every single thing you spend money on. This means everything - from big purchases to that pack of gum you bought at the checkout. Don't leave anything out, no matter how small it seems.

The goal is to see exactly where your money is going. Many people are surprised when they do this. You might find you're spending more in certain areas than you realized.

Remember, this isn't about judging your spending. It's about understanding it. Be honest with yourself during this process. It's the best way to get a true picture of your financial habits.

Fun Fact: People who track their spending often find they're spending 20% more than they thought.

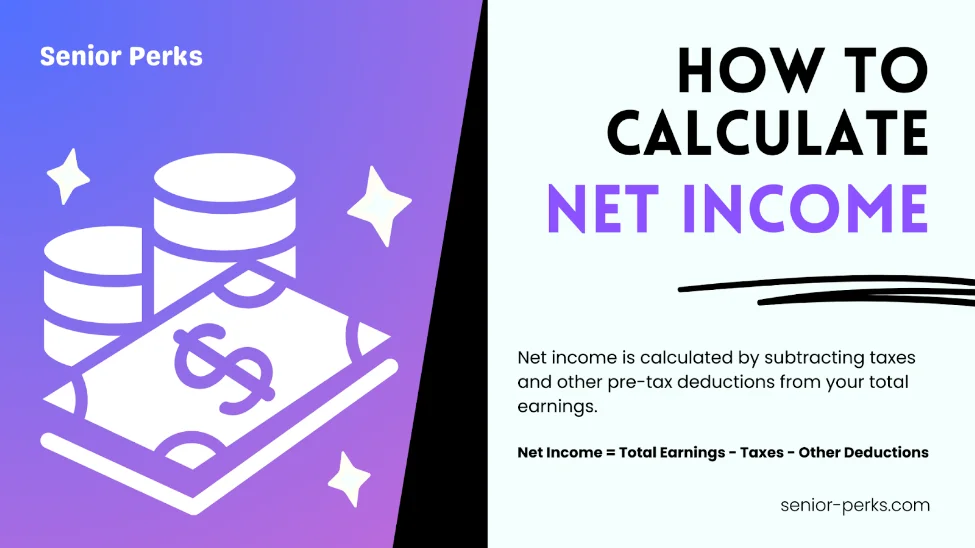

3. Calculate your net income accurately

Many people make the mistake of budgeting with their gross income - the amount they earn before taxes and other deductions. This can lead to overspending because you're working with money you don't actually have in your pocket.

Let's say your gross income is $4,000 a month. But after taxes, insurance, and retirement contributions, you only take home $3,200. If you budget based on $4,000, you might overspend by $800 each month!

Always check your pay stub or bank deposits to see your real take-home pay. This is the number you should use for your budget. It gives you a true picture of your spending power and helps keep your budget realistic.

4. Choose a budgeting method that fits you

There are many ways to budget, Think about your personality and goals when choosing. Are you detail-oriented or do you prefer a big-picture view? Do you need strict limits or more flexibility? Consider how much control you want and how much effort you're willing to put into budgeting. Finally, find a system that you can easily keep track of.

You can start with the 50-30-20 method which allocates your income into three categories: 50% for needs, 30% for wants, and 20% for savings. It can help you prioritize your spending and make better decisions.

Try a method for a few months. If it's not working, it's okay to switch to another. The best budget is one you'll actually use.

Check out our detailed guide to creating a budget.

5. Automate your savings

Make saving easier by setting it on autopilot. You can set up your bank account to automatically transfer money to your savings account each payday. This way, you save before you have a chance to spend.

A study by Case Western Reserve University found that automated savings are most beneficial for those with the lowest incomes and tightest budgets.

When the money moves to savings automatically, you're less likely to miss it or be tempted to spend it. It's a simple way to build your savings without having to think about it every month.

6. Use cash for discretionary spending

Try using cash for things like entertainment, dining out, or shopping. Using cash increases a phenomenon known as the "pain of paying," where consumers feel psychological discomfort when spending money. This pain is reduced when using credit cards, potentially leading to higher spending. Because it doesn't feel as "real" as handing over cash

Take out a set amount of cash each week for these expenses. When the cash is gone, you know you've reached your limit. For example, if you budget $100 for eating out, take that amount in cash at the start of the week. Once it's gone, you've hit your limit for restaurant meals.

Did you know:

52% of people are more likely to make an impulse purchase when paying with a card, compared to just 24% with cash.

(source: Forbes Advisor)

7. Implement zero-based budgeting

Zero-based budgeting means giving every dollar a job. Basically, you need to make your income minus your expenses equal zero. List all your income for the month. Then, assign each dollar to a category until you've used up all your income. Categories can include bills, savings, debt payments, and fun money.

For example, if you earn $3,000 a month, you might budget $1,000 for rent, $500 for groceries, $300 for savings, and so on until you've assigned all $3,000.

This method helps you be intentional with your money. It can prevent overspending and make sure you're using your money in ways that matter to you.

8. Use budgeting apps or spreadsheets for tracking

Technology can make budgeting easier and more accurate. Budgeting apps can help you keep track of your income and expenses.

To find the best tool for you, look at comparison websites. They often review different apps and software, looking at things like features, cost, and ease of use. Many also offer suggestions based on your specific needs.

Popular tools include YNAB (You Need A Budget), which uses zero-based budgeting principles to help you allocate every dollar. Rocket Money offers expense tracking and even helps negotiate bills on your behalf.

If you prefer more control, try using a spreadsheet. You can make your own budget layout with programs like Excel or Google Sheets. Many free budgeting templates are also available online, which can be helpful, especially if you are a beginner.

9. Make forward-looking budget

When you make your budget, don't just think about today. Look ahead to future expenses, too. This helps you avoid surprises and money stress later on. You can't predict everything, but thinking ahead can help you be ready for big expenses. It's about being prepared, not perfect.

For example, if you know your car needs new tires in six months, start saving a little each month now.

10. Create multiple budget scenarios

Planning for different financial situations can help you be ready for anything. Try making three budget scenarios: best-case, worst-case, and most likely.

For your best-case scenario, imagine everything goes well. Maybe you get a raise, or your business does better than expected. In the worst-case scenario, think about what could go wrong, like unexpected expenses or a drop in income. The most likely scenario is somewhere in between.

For example, if you're planning a vacation, your best case might be finding great deals on flights and hotels. The worst case could be higher prices and extra fees. ‘Most likely’ would be average prices based on your research.

Did you know:

In the U.S. Economic Well-Being Survey (2023-2024), 65% of adults said that price increases compared to the prior year worsened their financial situation.

11. Don’t do it alone

If you are managing finances as a family, involving everyone in the budgeting process will make it more effective and teach good money habits.

Sit down together and talk about your goals. Let each person share what's important to them. Maybe your partner wants to save up for a vacation, while your kids want new bikes. Kids can develop important financial skills early by participating in budgeting. Try to find a balance that works for everyone.

You could have a family meeting once a month to review the budget. Give each person a say in how to allocate any extra money or where to cut back if needed.

Did you know:

“Children make significant progress in economic understanding between the ages of 6 and 12, such that their understanding becomes ‘essentially adult’ around age 12.”

(source: Center For Financial Security research)

12. Apply opportunity cost analysis to spending decisions

When you're deciding how to spend your money, think about what you're giving up. This is called opportunity cost. It helps you make smarter choices with your budget.

For example, if you're thinking about buying a new $1,000 TV, consider what else you could do with that money. You could put it towards your emergency fund, invest it, or take a weekend trip. The opportunity cost is whatever you decide not to do.

Fun Fact: People who consider opportunity costs tend to save more money than those who don't think about opportunity costs.

13. Don't compare your budget to others

If you look at how others spend money, you might feel like you're falling behind. But remember that everyone's situation is different. What works for someone else might not work for you.

Social media often only shows the highlights of people's lives. You might see vacation photos or new purchases, but not the everyday budgeting behind the scenes. So, Instead of comparing, focus on your own goals. Your budget should reflect your priorities, not someone else's.

14. Celebrate small victories

When you're working on your budget, don't wait for big milestones to feel good about your progress. Celebrate the small wins along the way. This can actually help you reach your bigger goals. A study in the Harvard Business Review found that recognizing progress, no matter how small, can boost motivation and productivity.

15. Find an accountability partner

Having someone to check in with about your budget can help you stay on track. People are more likely to meet a goal after committing to someone else. With money goals, this accountability can make a big difference. Look for someone trustworthy who won't judge your financial situation.

16. Budget for personal growth and education

Set aside a specific percentage of your income for education and skill development. This investment in yourself can significantly boost your earning potential and career prospects. Aim for at least 5% of your after-tax income as a starting point. This should cover books, online courses, workshops, or formal education programs.

Take advantage of free or low-cost resources to maximize your learning budget. Utilize public libraries, free online courses from platforms like Coursera or edX, and any employer-sponsored training programs.

17. Include a "fun" category in your budget

A balanced budget includes both responsible saving and mindful spending on enjoyment. Without this balance, you're more likely to abandon your budget altogether. Allocate a specific amount for enjoyment in your budget.

Spend 5-10% of your after-tax income on fun activities, such as hobbies, entertainment, dining out, or other non-essentials.

Use the "envelope method" for your fun money. At the beginning of each month, withdraw the budgeted amount in cash and place it in an envelope.

Once it's gone, stop discretionary spending until the next month.

18. Beware of lifestyle creep and impulse purchases

Your spending increases as your income rises. Implement a 30-day waiting period for non-essential purchases over a certain amount, such as $100. This cooling-off period helps distinguish between genuine needs and impulsive wants.

It is highly recommended that you allocate at least 50% of your income increases to savings and investments immediately after a raise in income. This ensures that your wealth grows rather than your expenses expand.

Reassess your budget to reflect your new income, but maintain your previous lifestyle for at least six months. This buffer period allows you to adjust your financial plan thoughtfully rather than succumbing to immediate lifestyle upgrades.

19. Avoid overly restrictive budget

You don't want to feel deprived, which increases the likelihood of giving up on your budget. Set realistic goals so you don't get frustrated.

Adopt a balanced approach that allows for occasional treats and unplanned expenses. Financial psychologists recommend the 80/20 rule: stick to your budget 80% of the time, allowing 20% for flexibility and indulgences.

20. Budget for healthcare costs and insurance

Prioritize healthcare expenses in your budget to protect both your physical and financial health. Set aside funds for insurance premiums, out-of-pocket costs, and potential medical emergencies. Factor in potential long-term care costs as you age.

Consider opening a Health Savings Account (HSA) if you have a high-deductible health plan. HSAs offer a triple tax advantage for U.S. residents:

Contributions are tax-deductible, reducing your taxable income.

Withdrawals for qualified medical expenses are tax-free.

Any investment earnings within the account grow tax-free.

For 2024, the IRS allows individuals to contribute up to $4,150 to an HSA, while families can contribute up to $8,300. If you are 55 and older, you can add an extra $1,000 as a catch-up contribution.

Estimate your annual healthcare expenses based on past usage and current health status. Include costs for prescriptions, regular check-ups, and any ongoing treatments. Taking this total and dividing it by 12 will give you your monthly healthcare budget.

Did you know:

70% of people over 65 will need some form of long-term care in their lifetime (Source: U.S. Department of Health and Human Services)

21. Include long-term goals

When creating your budget, don't just focus on immediate expenses. Integrate long-term financial planning to ensure your current spending aligns with your future goals.

Start by identifying your long-term financial objectives, such as retirement, buying a home, or funding your children's education. Then, allocate a portion of your current income towards these goals in your monthly budget.

Make sure you have a separate "sinking fund" for future expenses that will allow you to save gradually for big-ticket items.

22. Conduct regular financial check-ins

Regularly take the time to assess your financial situation and progress towards your goals, ideally monthly or quarterly. This will help you stay on track with your finances and make the necessary adjustments in a timely manner.

If you're in a relationship, involve your partner in these check-ins. Open communication about finances can strengthen your relationship and ensure you're both aligned on financial goals.

23. Prioritize debt repayment

Prioritize your highest interest rate debts first to minimize interest costs. Credit cards often have the highest interest rates. Allocate any extra funds in your budget towards debt repayment.

Implement the debt avalanche method that focuses on paying off the debt with the highest interest rate while making minimum payments on others. This approach saves the most money in interest over time.

Review your expenses critically and redirect unnecessary spending to debt payments.

24. Create an emergency fund

You never know when something unexpected will happen. A contingency plan will help you handle these things without panicking, and you won't need to use credit cards or borrow money. Think about things that may go wrong, like losing your job or having to pay a large medical bill.

A good plan usually includes saving enough money to cover 3-6 months of your regular bills. This gives you time to figure things out if something big happens, like losing your job.

Did you Know:

59% of Americans are not comfortable with their emergency savings.

(source: Bankrate)

25. Adapt your budget regularly

A budget that worked for you last year might not be suitable now. Life doesn't stand still, and neither should your budget. Major life events like getting married, having a child, or changing jobs can significantly impact your finances.

Review your budget at least every 3-6 months or after any major life change and adjust it according to your income and expenses. This will help you stay in control of your finances and goals.

Bottom Line

With practice, budgeting becomes easier. Start today, put these tips into action, be patient with yourself, and watch as your financial confidence grows. Your future self will thank you for the efforts you are making now.

Stay tuned for more money management tips and information.